Good morning, traders…

It’s official…

The Federal Reserve cut interest rates by 25 basis points on Wednesday.

This is the third cut in the recent cycle, with rates now sitting at 3.50%–3.75%.

But while the news remains focused on the headline rate cut, I’m more intrigued by Jerome Powell’s press conference.

The “what” is just a number. I want to understand the “why.”

For those listening closely, Powell gave some major hints, laying breadcrumbs for what the next 4-6 months might look like.

Make no mistake: The Fed’s path forward determines how the market behaves.

Rate cuts typically fuel rallies. But Powell’s comments suggest something more nuanced is happening.

You need to read between the lines to understand what Powell actually hinted at (not what the headlines claimed)…

Then use those hints to inform your trading approach for 2026 (and beyond).

J. Powell Just Revealed More Than You Think…

Why The Fed Cut Now

Powell framed the decision as a balanced-risk response.

The labor market continued cooling slightly more than expected.

Inflation (excluding tariff effects) is drifting into the low 2% range.

Goods inflation is almost entirely tariff-driven, which Powell expects to be a one-time price-level increase rather than an ongoing inflation spiral.

No signs of an overheated economy appeared in the data.

Upside risks to inflation remain, but mostly from tariffs.

Downside risks to employment have grown, with job creation potentially negative.

The Committee sees the policy rate as now within the “broad range of neutral.”

Long story short: They cut because inflation is cooling and the labor market is shaky.

Yet Powell repeated the same line he said at the last meeting, verbatim:

“There is no risk-free policy path.”

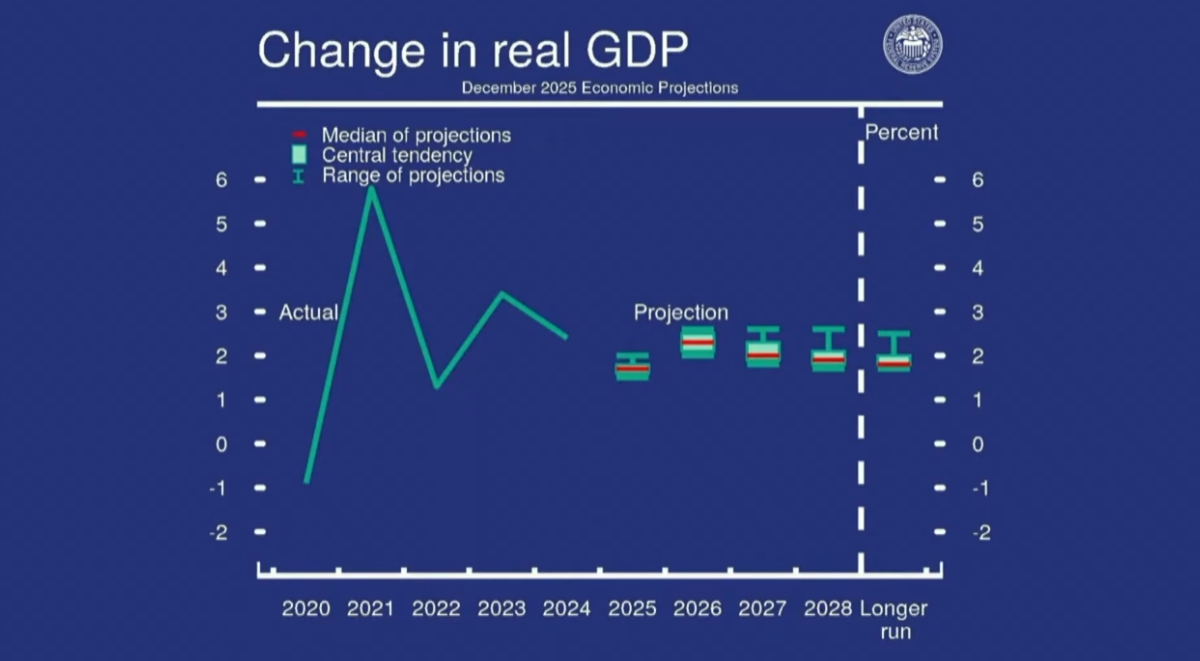

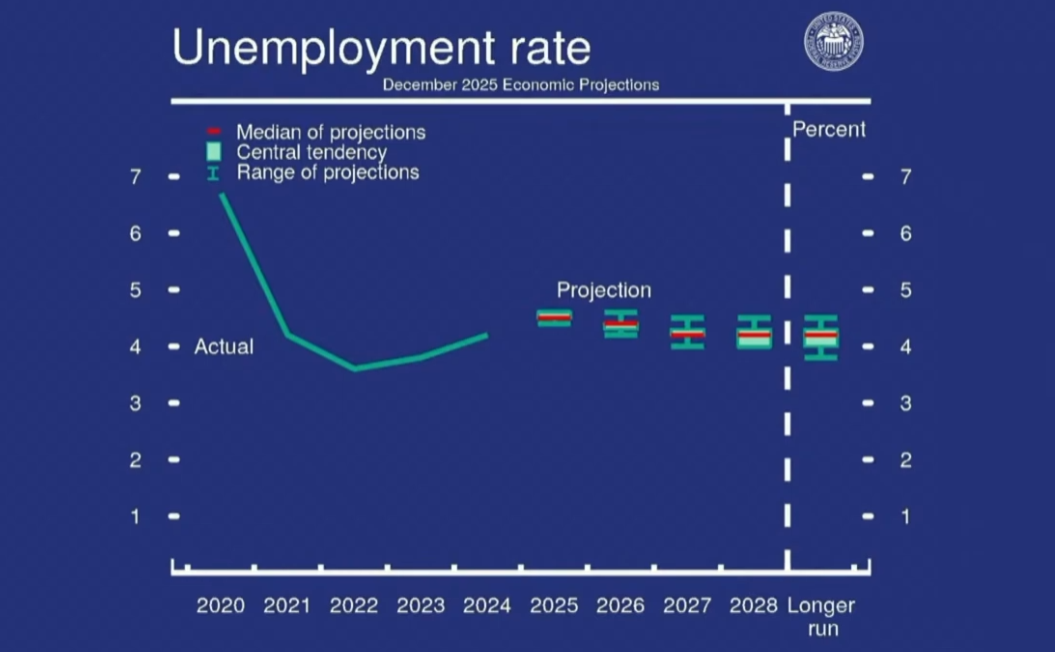

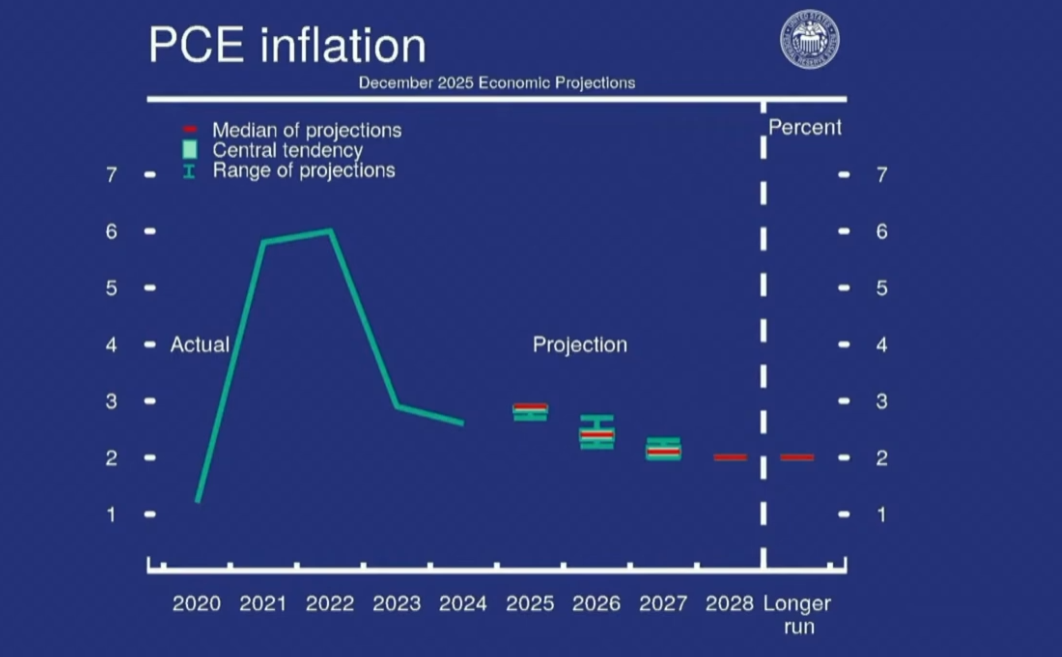

What The Economic Projections Show

The Growth Outlook

- Government data is still delayed due to the shutdown, but private indicators suggest moderate GDP expansion.

- Consumer spending remains solid.

- Business investment continues to grow.

- Housing activity remains weak.

- The shutdown likely weighed on the current quarter but should reverse next quarter.

- SEP projects real GDP rising 1.7% in 2024 and 2.3% in 2025.

- Some of next year’s growth reflects timing distortions from the shutdown.

The Labor Market Outlook

- The labor market is cooling gradually…

- Layoffs remain low.

- Hiring difficulty has eased.

- Surveys show declining job availability.

- The unemployment rate in the latest official report was 4.4%, up from earlier levels.

- Job gains have slowed significantly over the year.

- The Fed believes payroll data overstates true job growth by roughly 60,000 per month.

- True job creation may be near zero or negative.

- Labor supply has weakened due to lower immigration and participation.

- Downside risks to employment have increased.

- SEP projects unemployment at 4.5% by year-end, then slightly lower thereafter.

The Inflation Outlook

- Inflation has eased sharply from its 2022 peak but remains somewhat above the 2% goal.

- Very little new inflation data has been reported since October.

- Headline PCE inflation and Core PCE Inflation are both at 2.8% year-over-year.

- Goods inflation has risen due to tariffs, while services inflation is cooling.

- Short-term inflation expectations have declined from their peaks.

- Long-term inflation expectations remain anchored around 2%.

- SEP projects PCE inflation at 2.9% in 2024 and 2.4% in 2025.

What Powell Said About Future Moves

There is no pre-set course.

Decisions remain meeting-by-meeting.

The Fed is now in a position to “wait and see” how the economy evolves.

The SEP median rate projection shows 3.4% for 2026 and 3.1% for 2027, unchanged from September.

Intriguing Answers From The Q&A

Q: Could the Fed’s next move be a hike?

Powell: Very unlikely. The discussion is between holding steady or cutting further, not hiking.

Q: Why is unemployment rising so slowly despite productivity growth?

Powell: Productivity gains allow higher GDP without much hiring. Labor supply shrinkage (immigration decline, participation softness) is a major factor.

Q: Is AI having a positive effect on economic productivity?

Powell: Productivity has been unusually strong (multi-year run near 2%). AI spending, especially in data centers, is supporting business investment and boosting GDP. But AI-driven job loss doesn’t yet show up in claims data. The long-run effects remain uncertain.

Q: Is tariff inflation peaking soon?

Powell: It likely peaks in Q1, then fades through late next year (assuming no new tariffs get announced).

Q: Any bright spots on the horizon for housing affordability?

Powell: Not really. Rate cuts alone won’t fix it. The problem is driven by a structural shortage coupled with mortgage-rate lock-in (“golden handcuffs”).

What This Means For Your Trading

As important as the macro side is, it doesn’t change my approach.

I don’t look at a 25 basis point cut (one that had a 90% probability of happening, mind you), and go “Oh, now I’ll trade completely differently!”

And that’s not what I suggest you do, either.

It’s more about reading the tea leaves to get an idea of where the market might be headed.

The Fed governors have more data, projections, and insight on the U.S. economy than anyone else in the world.

To not listen to them would be foolish.

The positive: The Fed is buying T-bills. Inflation is going in the right direction. Growth is above expectations.

Those are major tailwinds for the stock market.

The negative: If Powell’s concerns about negative job growth materialize, the market will reprice growth expectations downward.

That’s a headwind to watch out for in 2026.

But as long as the labor market holds and inflation continues trending toward 2%, my view remains unchanged:

The most likely direction for the market is up.

Happy trading,

Ben Sturgill

*Past performance does not indicate future results