The stock goes up, your call loses money.

Sound familiar? It’s one of the most frustrating experiences in options.

There’s a reason that happens. Time decay was working against you.

While you were focused on watching the chart move, it was eating the part of your premium that had nothing to do with whether you were right about the stock.

A buddy of mine who’s just getting into options came to me with this one last week:

He’d bought a $105 call, 30 days out, on a stock trading around $100.

He paid $2.10 for the contract. Three weeks passed.

My buddy was confused. He asked me, “If the stock is above my strike with ten days left, why is the contract barely worth more than when I bought it?”

Let me explain…

100 Shares You’ll Never Own

Before I explained, I asked him: “Do you know what you bought?”

He started to answer, then trailed off. Something about the right to buy shares at $105. Or maybe the $2.10 he’d put down betting on the move. He wasn’t sure which.

That’s where it started unraveling. I had to bring him back to the basics first.

A call option is a contract. It gives you the right to buy 100 shares of the underlying at your strike, on or before expiration.

So that $2.10 premium he paid? One contract covers 100 shares, which means he’d put $210 on the table. And if he exercised at $105, he’d be buying $10,500 worth of stock.

Retail traders almost never exercise their contracts.

The contract itself trades on the open market. If it gains value, you sell it and pocket the difference. The right to those shares is what gives the contract its value, but what you trade is the contract.

The shares set the math. Contracts are where the trade happens.

The Two Halves

The other piece of the puzzle was inside the $210 itself. That premium had two prices baked into it.

Intrinsic value is what the contract would be worth if you exercised it this second. His $105 call with the stock at $100 has zero intrinsic value. Even when the stock eventually climbed above $105, intrinsic value was barely off the floor. The stock was just a dollar or two past the strike.

Extrinsic value is everything else. Time until expiration and the volatility the market is pricing in. Together, they’re the market’s estimate of whether the stock will get somewhere interesting before expiration.

When he bought that $105 call with the stock at $100, every dollar of his $210 was extrinsic. Nothing he’d paid for was anchored to the current price of the stock.

Only Half of It Melts

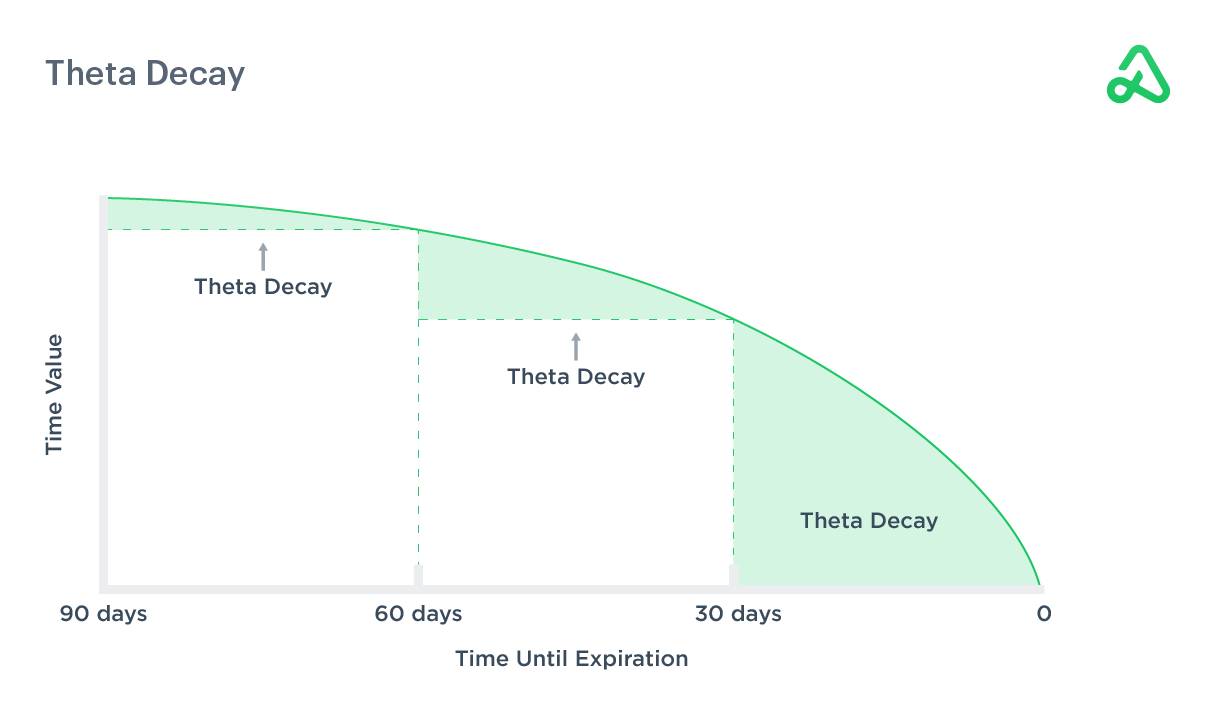

Time decay only eats extrinsic value.

Walk through his trade. Entry: $210, all extrinsic. Twenty days later, the stock finally touches $105. The contract might now be worth, call it, $150. He nailed the direction. He’s down on the position.

Intrinsic value at $105 is basically zero. Twenty days of extrinsic have melted off. He was right about the direction and still down on the trade.

For the trade to pay, the stock has to push meaningfully past $105 in the ten days left. Touching the strike isn’t enough this late in the contract. Twenty days ago, hitting $105 would have paid him. Most of the extrinsic value has already melted off.

This is why decay accelerates in the last stretch. The remaining extrinsic value has less and less time to be worth anything, so it evaporates faster in the final two weeks than it did in the first two.

When you buy a call, you’re predicting where the stock goes. You’re also predicting when it gets there. Time decay is the reason the second prediction matters as much as the first.

What This Means For Your Trading

Sizing a call is a two-part decision: how much time, and how far from the money.

On time: if you think a setup plays out in two weeks, buy a monthly contract, not a weekly. The extra premium you pay for the time buffer protects you from the acceleration in the final stretch. Running out of time is the most expensive mistake in options.

On strike: close-to-the-money gives you intrinsic value faster. Far-OTM gives you leverage. But decay is what makes the far-OTM bet harder.

Every call is a bet on both. Trade the clock, not just the chart.

Be good (and be good to others),

Ben Sturgill

*Past performance does not indicate future results